FOR SALE

→1620 Stanton Ave

$640,999

San Pablo

1620 Stanton Avenue

3 Bedrooms | 2 Baths | 1,227 sq. ft.

Offered for: $640,999

-

MLS #326019315

-

3 bedrooms

-

2 full bathrooms

-

1,227 square feet

-

Built in 1964

-

Single-level ranch home

-

9,200 sq ft lot

-

Bay views

-

Large private backyard

-

Mature fruit trees

-

Brick wood-burning fireplace

-

Central heating and cooling

-

Laminate flooring

-

Breakfast area kitchen

-

Attached 2-car garage

-

Interior garage access

-

RV or boat parking

-

Level driveway

-

Fenced yard

-

Uncovered deck and patio

-

Shed storage included

-

Public sewer and water

-

Convenient commuter location

-

Trust sale opportunity

Every Home Has a Story-Experience This One

At Navigate Real Estate, we believe every home deserves to have its story told. To the right, you'll find an interactive digital booklet that brings this property to life. Take the tour and explore every detail-from standout features and modern comforts to the neighborhood amenities that make this area such a great place to call home. Click now to watch the story and see if this could be your next chapter.

Click the image to the right and read this home's story.

WHO YOU WORK WITH MATTERS

EMelinda and Kaily

DRE Lic# 01726029

DRE Lic# 02224415

The Capp family are fourth- and fifth-generation wine growers in the Suisun Valley, where their name has long been synonymous with agriculture, grapes, and winemaking.

With nearly 20 years in the title and mortgage industry and over 16 years of real estate sales experience, Melinda and Kaily Capp bring deep market knowledge and genuine passion to every transaction. Backed by Navigate Real Estate and the RESAAS global network of 436,000 agents across 100+ countries, your home receives true worldwide exposure.

"Every home has a story—and we’d love to tell yours." With clear communication, patience, and local expertise, The Capp Team empowers clients to make confident decisions. Whether buying, selling, or investing, expect a perfect blend of professionalism, creativity, and dedication to achieving your real estate goals

TESTIMONIALS

WHAT OUR HAPPY CLIENTS SAY...

"Melinda Capp is a great agent. She made sure I understood all the paperwork and she answered all of my questions. Melinda also helped me purchase my first home under the asking price. She treated me like family. I can’t wait to purchase my second home. If you’re buying a home make sure you contact Melinda Capp!"

-CLIFF COOL

"Melinda is awesome at what she does. She helped my husband and I buy our first home in 2010 and recently helped us sale our home in 2017. She is very knowledgeable, professional and overall great person."

-Shermeka Jones

"Melinda was so wonderful throughout the whole process of buying my first home. She helped me close on my dream home in 15 days! She was fast with the paperwork and always available for any questions or assistance. I would highly recommend Melinda to anyone looking to buy or sell a home!"

-Haley Hull

FOR SALE

→915 Liberty Dr

$575,000

Suisun City

915 Liberty Dr

4 Bedrooms | 2.5 Baths | 2,030 sq. ft.

Offered for: $575,000

-

MLS #325092875

-

4 Bedrooms

-

3 Bathrooms (2 Full, 1 Half)

-

2,030 Sq Ft

-

Built in 2005

-

Price: $575,000

-

Lot Size: 0.0716 Acres

-

Two-Story Design

-

Traditional Architectural Style

-

Central Heating & Cooling

-

Fireplace in Living Room

-

Fresh Paint Throughout

-

New Carpet Installed

-

Updated Interior Finishes

-

Island Kitchen

-

Gas Range & Dishwasher

-

Upstairs Laundry Room

-

Primary Suite with Soaking Tub

-

Double Sink Vanity

-

Low-Maintenance Backyard

-

Attached 2-Car Garage

-

Near Suisun Marina & Waterfront

-

Close to Shopping & Schools

-

Vacant and Easy to Show

Every Home Has a Story-Experience This One

At Navigate Real Estate, we believe every home deserves to have its story told. To the right, you'll find an interactive digital booklet that brings this property to life. Take the tour and explore every detail-from standout features and modern comforts to the neighborhood amenities that make this area such a great place to call home. Click now to watch the story and see if this could be your next chapter.

Click the image to the right and read this home's story.

WHO YOU WORK WITH MATTERS

EMelinda and Kaily

DRE Lic# 01726029

DRE Lic# 02224415

The Capp family are fourth- and fifth-generation wine growers in the Suisun Valley, where their name has long been synonymous with agriculture, grapes, and winemaking.

With nearly 20 years in the title and mortgage industry and over 16 years of real estate sales experience, Melinda and Kaily Capp bring deep market knowledge and genuine passion to every transaction. Backed by Navigate Real Estate and the RESAAS global network of 436,000 agents across 100+ countries, your home receives true worldwide exposure.

"Every home has a story—and we’d love to tell yours." With clear communication, patience, and local expertise, The Capp Team empowers clients to make confident decisions. Whether buying, selling, or investing, expect a perfect blend of professionalism, creativity, and dedication to achieving your real estate goals

TESTIMONIALS

WHAT OUR HAPPY CLIENTS SAY...

"Melinda Capp is a great agent. She made sure I understood all the paperwork and she answered all of my questions. Melinda also helped me purchase my first home under the asking price. She treated me like family. I can’t wait to purchase my second home. If you’re buying a home make sure you contact Melinda Capp!"

-CLIFF COOL

"Melinda is awesome at what she does. She helped my husband and I buy our first home in 2010 and recently helped us sale our home in 2017. She is very knowledgeable, professional and overall great person."

-Shermeka Jones

"Melinda was so wonderful throughout the whole process of buying my first home. She helped me close on my dream home in 15 days! She was fast with the paperwork and always available for any questions or assistance. I would highly recommend Melinda to anyone looking to buy or sell a home!"

-Haley Hull

FOR SALE

→ 67 Zinnia Ln - Napa

$529,900

Napa County

67 Zinnia Lane

Offered for $529,900

4 Bedrooms | 3 Baths | 2,714 sq. ft.

- MLS ID:324079937

- 4 Bedrooms

- 3 Baths

- 2,714 sq. ft.

- +/- 1/2 Acre Lot

- Development: Circle Oaks

- HOA: Yes

- Topography: Woods & Hills

- Open Concept

- Investment Opportunity

- Flip it - Keep It

- Rustic Charm

- Wood Burning Stove

- Multiple Building Sites

- Open Concept Layout

- Lots of Natural Light

- Downstairs Development Potential

- Potential AirBnB

- Between Napa and Solano Counties

- Views

Charming Country Fixer - A Rare Investment Opportunity in the Heart of Circle Oaks

Every home has a story, and this one is ready for its next chapter—waiting for you to shape its future. Nestled on a serene ½-acre lot, this property offers an enchanting retreat with endless potential. With just a bit of TLC, this diamond in the rough can become a bespoke country oasis, whether as a primary residence, a vacation getaway, or a lucrative investment property.

The main living space welcomes you with rustic charm, featuring a cozy wood-burning stove and an open-concept layout, while natural light pours through the windows, creating a warm, inviting ambiance. The kitchen offers rustic appeal, with plenty of space for culinary creativity. Downstairs, a partially finished lower level hints at exciting possibilities—transform it into an in-law unit with a private entrance and kitchenette, ideal for multi-generational living or rental income.

Step outside to discover two spacious decks, each a perfect setting for morning coffee, evening cocktails, or gatherings with friends, all set against the breathtaking countryside views. The outdoors becomes an extension of your living space, where you can immerse yourself in nature's beauty.

Discover Life in Circle Oaks

Tucked within the rolling hills of Napa County, Circle Oaks is an unincorporated community that offers a unique blend of rustic tranquility and proximity to the best of wine country. Located just 15 minutes from downtown Napa, this area provides a peaceful escape without sacrificing easy access to renowned restaurants, boutique shopping, and cultural attractions. Nearby, the scenic landscapes of Gordon Valley and Wooden Valley invite you to explore local wineries, creating opportunities for weekend adventures.

WHO YOU WORK WITH MATTERS

Emily, Melinda and Kaily

DRE Lic# 01726029

DRE Lic# 02153614

DRE Lic# 02224415

The Capp's are fourth and fifth generation wine growers in the Suisun Valley wine region. The Capp family name has been synonymous with agriculture, grapes and wine. Spending almost 20 years in the title and mortgage industry Melinda, Emily and Kaily Capp bring over 16 years combined real estate sales experience. Backed by NavigateRE and the RESAAS reach of over 436,000 agents in over 100+ countries you can trust your home will gain true global exposure.

"Every home has a unique story and we would like the opportunity to tell yours. With a focused approach of analysis, communication, perseverance and patience that sets us apart from our peers. The Capp and Capp team listens to their clients, then using their extensive knowledge of inventory, financing and contacts, they empower their clients to make informed, satisfying decisions."

If you live here already, you know how blessed we are. If you’re considering living or investing here, you’ve probably experienced some of the area’s extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Solano and Napa Counties are your real estate destination, you’ve arrived at the right spot. Whether you’re looking to buy your first home – or to sell an estate – expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

TESTIMONIALS

WHAT OUR HAPPY CLIENTS SAY...

"Melinda Capp is a great agent. She made sure I understood all the paperwork and she answered all of my questions. Melinda also helped me purchase my first home under the asking price. She treated me like family. I can’t wait to purchase my second home. If you’re buying a home make sure you contact Melinda Capp!"

-CLIFF COOL

"Melinda is awesome at what she does. She helped my husband and I buy our first home in 2010 and recently helped us sale our home in 2017. She is very knowledgeable, professional and overall great person."

-Shermeka Jones

"Melinda was so wonderful throughout the whole process of buying my first home. She helped me close on my dream home in 15 days! She was fast with the paperwork and always available for any questions or assistance. I would highly recommend Melinda to anyone looking to buy or sell a home!"

-Haley Hull

FOR SALE

→ +/-131 Acres Quail Ridge - Napa

$2,500,000

Napa

Quail Ridge Road

+/- 131 Acres Land

Offered for $2,500,000

+/- 131 Acre Lot

Prime Development

Multiple Building Sites

360 Degree Views

$2,500,000

Every Home Has a Story, and yours awaits to be unveiled on this Expansive Lot! Situated within the heart of this coveted neighborhood lies a true gem, Here, you'll discover an opportunity to actualize the lifestyle you've always envisioned—a pristine canvas awaiting your discerning touch.

Envision stepping beyond the threshold into your own personal sanctuary, where the horizons of possibility stretch as far as the eye can see. Transform this sprawling lot into a verdant garden retreat, adorned with flourishing flora and serene water features. Imagine cultivating a thriving vegetable garden, reaping the rewards of your labor with each abundant harvest. Alternatively, picture a tranquil outdoor haven, offering respite from the demands of daily life amidst the tranquility of your private domain.

Embrace the journey of homeownership and embark on an odyssey brimming with limitless possibilities and untapped potential. From intimate gatherings with loved ones to moments of quiet contemplation, this is where your narrative truly begins. Welcome home to a place where dreams take root and legacies are forged—your story starts here!"

MLS ID: 324078600

+/- 131 Acres

Development Site

Multiple Building Sites

Gated Property

Views: Bay, Bridges, City, Mountains, Orchard, Panoramic, Ridge, Valley, Vineyard

Roads: Dirt, Paved

Topographry: Woods Topography, Gently Sloped, Hillside, Hilltop, Hilly, Rolling, Trees

Electricity: At Lot Line

Gordon Valley - Napa County

Development Status: Building Site Cleared

MLS ID: 324078600

+/- 131 Acres

Development Site

Multiple Building Sites

Gated Property

Views: Bay, Bridges, City, Mountains, Orchard, Panoramic, Ridge, Valley, Vineyard

Roads: Dirt, Paved

Topographry: Woods Topography, Gently Sloped, Hillside, Hilltop, Hilly, Rolling, Trees

Electricity: At Lot Line

Gordon Valley - Napa County

Development Status: Building Site Cleared

WHO YOU WORK WITH MATTERS

Emily, Melinda and Kaily

DRE Lic# 01726029

DRE Lic# 02153614

DRE Lic# 02224415

The Capp's are fourth and fifth generation wine growers in the Suisun Valley wine region. The Capp family name has been synonymous with agriculture, grapes and wine. Spending almost 20 years in the title and mortgage industry Melinda, Emily and Kaily Capp bring over 16 years combined real estate sales experience. Backed by NavigateRE and the RESAAS reach of over 436,000 agents in over 100+ countries you can trust your home will gain true global exposure.

"Every home has a unique story and we would like the opportunity to tell yours. With a focused approach of analysis, communication, perseverance and patience that sets us apart from our peers. The Capp and Capp team listens to their clients, then using their extensive knowledge of inventory, financing and contacts, they empower their clients to make informed, satisfying decisions."

If you live here already, you know how blessed we are. If you’re considering living or investing here, you’ve probably experienced some of the area’s extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Solano and Napa Counties are your real estate destination, you’ve arrived at the right spot. Whether you’re looking to buy your first home – or to sell an estate – expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

TESTIMONIALS

WHAT OUR HAPPY CLIENTS SAY...

"Melinda Capp is a great agent. She made sure I understood all the paperwork and she answered all of my questions. Melinda also helped me purchase my first home under the asking price. She treated me like family. I can’t wait to purchase my second home. If you’re buying a home make sure you contact Melinda Capp!"

-CLIFF COOL

"Melinda is awesome at what she does. She helped my husband and I buy our first home in 2010 and recently helped us sale our home in 2017. She is very knowledgeable, professional and overall great person."

-Shermeka Jones

"Melinda was so wonderful throughout the whole process of buying my first home. She helped me close on my dream home in 15 days! She was fast with the paperwork and always available for any questions or assistance. I would highly recommend Melinda to anyone looking to buy or sell a home!"

-Haley Hull

SOLD

→ 156 Lakewood Ave., Vallejo

$550,000

🛏 3 Bedrooms

🛁 1 Bathrooms

🔲 1,132 sq. ft.

🗓️ Year Built 1954

💲 535,000

Every Home Has a Story, and yours awaits to be unveiled on this Expansive Lot! Situated within the heart of this coveted neighborhood lies a true gem, Here, you'll discover an opportunity to actualize the lifestyle you've always envisioned—a pristine canvas awaiting your discerning touch.

Envision stepping beyond the threshold into your own personal sanctuary, where the horizons of possibility stretch as far as the eye can see. Transform this sprawling lot into a verdant garden retreat, adorned with flourishing flora and serene water features. Imagine cultivating a thriving vegetable garden, reaping the rewards of your labor with each abundant harvest. Alternatively, picture a tranquil outdoor haven, offering respite from the demands of daily life amidst the tranquility of your private domain.

Embrace the journey of homeownership and embark on an odyssey brimming with limitless possibilities and untapped potential. From intimate gatherings with loved ones to moments of quiet contemplation, this is where your narrative truly begins. Welcome home to a place where dreams take root and legacies are forged—your story starts here!"

| MLS ID: 324019519

Bedrooms: 3 Bathrooms: 1 Square Feet: 1,132 Year Built: 1954 |

Lot Size: 11,326 sq. ft.

Subdivision: Castlewood Gardens Size: Single Story Parking: 2 Car Garage HOA: No |

- Fireplace

- Wood like Floors

- Microwave

- Stove

- Oven

- Dishwasher

- Open Living

- Updated Kitchen

- Backyard Deck

- Shed

- Large Patio

- Provacy

WHO YOU WORK WITH MATTERS

Emily, Melinda and Kaily

DRE Lic# 01726029

DRE Lic# 02153614

DRE Lic# 02224415

The Capp's are fourth and fifth generation wine growers in the Suisun Valley wine region. The Capp family name has been synonymous with agriculture, grapes and wine. Spending almost 20 years in the title and mortgage industry Melinda, Emily and Kaily Capp bring over 16 years combined real estate sales experience. Backed by NavigateRE and the RESAAS reach of over 436,000 agents in over 100+ countries you can trust your home will gain true global exposure.

"Every home has a unique story and we would like the opportunity to tell yours. With a focused approach of analysis, communication, perseverance and patience that sets us apart from our peers. The Capp and Capp team listens to their clients, then using their extensive knowledge of inventory, financing and contacts, they empower their clients to make informed, satisfying decisions."

If you live here already, you know how blessed we are. If you’re considering living or investing here, you’ve probably experienced some of the area’s extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Solano and Napa Counties are your real estate destination, you’ve arrived at the right spot. Whether you’re looking to buy your first home – or to sell an estate – expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

TESTIMONIALS

WHAT OUR HAPPY CLIENTS SAY...

"Melinda Capp is a great agent. She made sure I understood all the paperwork and she answered all of my questions. Melinda also helped me purchase my first home under the asking price. She treated me like family. I can’t wait to purchase my second home. If you’re buying a home make sure you contact Melinda Capp!"

-CLIFF COOL

"Melinda is awesome at what she does. She helped my husband and I buy our first home in 2010 and recently helped us sale our home in 2017. She is very knowledgeable, professional and overall great person."

-Shermeka Jones

"Melinda was so wonderful throughout the whole process of buying my first home. She helped me close on my dream home in 15 days! She was fast with the paperwork and always available for any questions or assistance. I would highly recommend Melinda to anyone looking to buy or sell a home!"

-Haley Hull

Why Overpricing Your House Can Cost You

If you’re trying to sell your house, you may be looking at this spring season as the sweet spot – and you’re not wrong. We’re still in a seller’s market because there are so few homes for sale right now. And historically, this is the time of year when more buyers move, and competition ticks up. That makes this an exciting time to put up that for sale sign.

But while conditions are great for sellers like you, you’ll still want to be strategic when it comes time to set your asking price. That’s because pricing your house too high may actually cost you in the long run.

The Downside of Overpricing Your House

The asking price for your house sends a message to potential buyers. From the moment they see your listing, the price and the photos are what’s going to make the biggest first impression. And, if it’s priced too high, you may turn people away. As an article from U.S. News Real Estate says:

“Even in a hot market where there are more buyers than houses available for sale, buyers aren't going to pay attention to a home with an inflated asking price.”

That’s because no homebuyer wants to pay more than they have to, especially not today. Many are already feeling the pinch on their budget due to ongoing home price appreciation and today’s mortgage rates. And if they think your house is overpriced, they may write it off without even stepping foot in the front door, or simply won’t make an offer if they think it’s priced too high.

If that happens, it’s going to take longer to sell. And ideally you don’t want to have to think about doing a price drop to try to re-ignite interest in your house. Why? Some buyers will see the price cut as a red flag and wonder why the price was reduced, or they’ll think something is wrong with the house the longer it sits. As an article from Forbes explains:

“It’s not only the price of an overpriced home that turns buyers off. There’s also another negative component that kicks in. . . . if your listing just sits there and accumulates days on the market, it will not be a good look. . . . buyers won’t necessarily ask anyone what’s wrong with the home. They’ll just assume that something is indeed wrong, and will skip over the property and view more recent listings.”

Your Agent’s Role in Setting the Right Price

Instead, pricing it at or just below current market value from the start is a much better strategy. So how do you find that ideal asking price? You lean on the pros. Only an agent has the expertise needed to research and figure out the current market value for your home.

They’ll factor in the condition of your house, any upgrades you’ve made, and what other houses like yours are selling for in your area. And they’ll use all of that information to find that target number. The right price will bring in more buyers and make it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly.

Bottom Line

Even though you want to bring in top dollar when you sell, setting the asking price too high may deter buyers and slow down the sales process.

Let’s connect to find the right price for your house, so we can maximize your profit and still draw in eager buyers willing to make competitive offers.

915 Liberty Dr, Suisun City, CA 94585

4 Bedroom | 3 Bath | 2,714 sq. ft. – $599,000

Read More

67 Zinnia Ln

4 Bedroom | 3 Bath | 2,714 sq. ft. – $599,000

Read More

Quail Ridge Dr

3 Bedroom | 1 Bath | 1,132 sq. ft. – $450,000

Read MoreWHO YOU WORK WITH MATTERS

Emily, Melinda and Kaily

DRE Lic# 01726029

DRE Lic# 02153614

DRE Lic# 02224415

The Capp's are fourth and fifth generation wine growers in the Suisun Valley wine region. The Capp family name has been synonymous with agriculture, grapes and wine. Spending almost 20 years in the title and mortgage industry Melinda, Emily and Kaily Capp bring over 16 years combined real estate sales experience. Backed by NavigateRE and the RESAAS reach of over 436,000 agents in over 100+ countries you can trust your home will gain true global exposure.

"Every home has a unique story and we would like the opportunity to tell yours. With a focused approach of analysis, communication, perseverance and patience that sets us apart from our peers. The Capp and Capp team listens to their clients, then using their extensive knowledge of inventory, financing and contacts, they empower their clients to make informed, satisfying decisions."

If you live here already, you know how blessed we are. If you’re considering living or investing here, you’ve probably experienced some of the area’s extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Solano and Napa Counties are your real estate destination, you’ve arrived at the right spot. Whether you’re looking to buy your first home – or to sell an estate – expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

TESTIMONIALS

WHAT OUR HAPPY CLIENTS SAY...

"Melinda Capp is a great agent. She made sure I understood all the paperwork and she answered all of my questions. Melinda also helped me purchase my first home under the asking price. She treated me like family. I can’t wait to purchase my second home. If you’re buying a home make sure you contact Melinda Capp!"

-CLIFF COOL

"Melinda is awesome at what she does. She helped my husband and I buy our first home in 2010 and recently helped us sale our home in 2017. She is very knowledgeable, professional and overall great person."

-Shermeka Jones

"Melinda was so wonderful throughout the whole process of buying my first home. She helped me close on my dream home in 15 days! She was fast with the paperwork and always available for any questions or assistance. I would highly recommend Melinda to anyone looking to buy or sell a home!"

-Haley Hull

If you want to buy a home, you should know your credit score is a critical piece of the puzzle when it comes to qualifying for a mortgage. Lenders review your credit to see if you typically make payments on time, pay back debts, and more. Your credit score can also help determine your mortgage rate. An article from US Bank explains:

“A credit score isn’t the only deciding factor on your mortgage application, but it’s a significant one. So, when you’re house shopping, it’s important to know where your credit stands and how to use it to get the best mortgage rate possible.”

That means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability. According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. The same article from US Bank explains:

“Your credit score (commonly called a FICO Score) can range from 300 at the low end to 850 at the high end. A score of 740 or above is generally considered very good, but you don’t need that score or above to buy a home.”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate you’re able to get. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

- Your Payment History: Late payments can have a negative impact by dropping your score. Focus on making payments on time and paying any existing late charges quickly.

- Your Debt Amount (relative to your credit limits): When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible.

- Credit Applications: If you’re looking to buy something, don’t apply for additional credit. When you apply for new credit, it could result in a hard inquiry on your credit that drops your score.

Bottom Line

Finding ways to make your credit score better could help you get a lower mortgage rate. If you want to learn more, talk to a trusted lender.

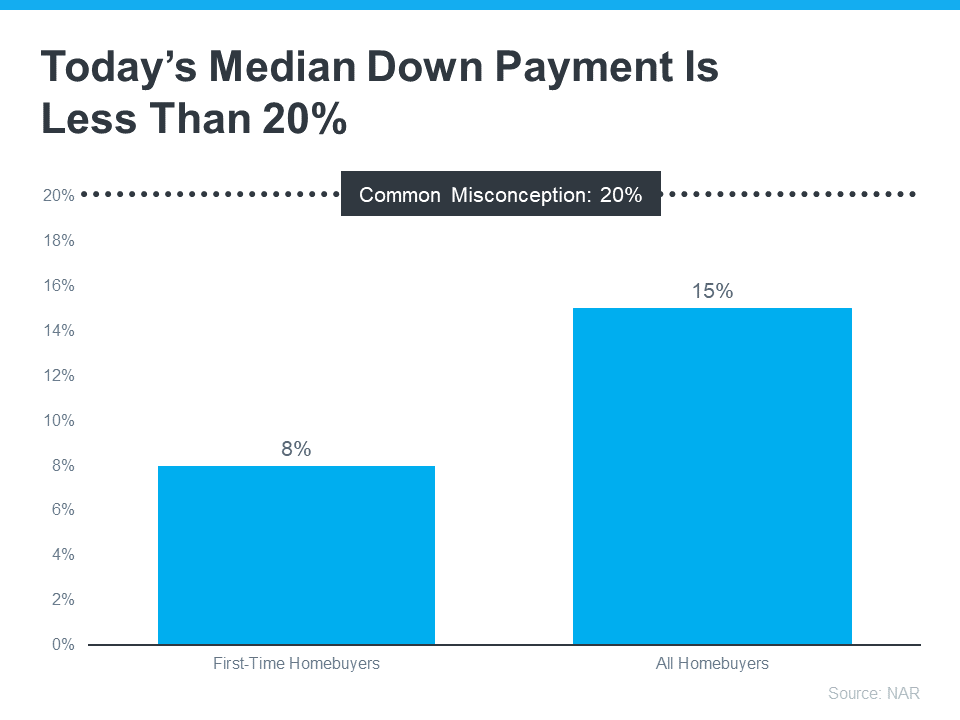

If you’re planning to buy your first home, saving up for all the costs involved can feel daunting, especially when it comes to the down payment. That might be because you’ve heard you need to save 20% of the home’s price to put down. Well, that isn’t necessarily the case.

Unless specified by your loan type or lender, it’s typically not required to put 20% down. That means you could be closer to your homebuying dream than you realize.

As The Mortgage Reports says:

“Although putting down 20% to avoid mortgage insurance is wise if affordable, it’s a myth that this is always necessary. In fact, most people opt for a much lower down payment.”

According to the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. In fact, for all homebuyers today it’s only 15%. And it’s even lower for first-time homebuyers at just 8% (see graph below):

The big takeaway? You may not need to save as much as you originally thought.

Learn About Resources That Can Help You Toward Your Goal

According to Down Payment Resource, there are also over 2,000 homebuyer assistance programs in the U.S., and many of them are intended to help with down payments.

Plus, there are loan options that can help too. For example, FHA loans offer down payments as low as 3.5%, while VA and USDA loans have no down payment requirements for qualified applicants.

With so many resources available to help with your down payment, the best way to find what you qualify for is by consulting with your loan officer or broker. They know about local grants and loan programs that may help you out.

Don’t let the misconception that you have to have 20% saved up hold you back. If you’re ready to become a homeowner, lean on the professionals to find resources that can help you make your dreams a reality. If you put your plans on hold until you’ve saved up 20%, it may actually cost you in the long run. According to U.S. Bank:

“. . . there are plenty of reasons why it might not be possible. For some, waiting to save up 20% for a down payment may “cost” too much time. While you’re saving for your down payment and paying rent, the price of your future home may go up.”

Home prices are expected to keep appreciating over the next 5 years – meaning your future home will likely go up in price the longer you wait. If you’re able to use these resources to buy now, that future price growth will help you build equity, rather than cost you more.

Bottom Line

Keep in mind that you don’t always need a 20% down payment to buy a home. If you’re looking to make a move this year, let’s connect to start the conversation about your homebuying goals.

Buying your first home is a big, exciting step and a major milestone that has the power to improve your life. As a first-time homebuyer, it’s a dream you can make come true, but there are some hurdles you’ll need to overcome in today’s housing market – specifically the limited supply of homes for sale and ongoing affordability challenges.

So, if you’re ready, willing, and able to buy your first home, here are three tips to help you turn your dream into a reality.

Save Money with First-Time Homebuyer Programs

Paying the initial costs of homeownership, like your down payment and closing costs, can feel a bit daunting. But there are many assistance programs for first-time homebuyers that can help you get a loan with little or no money upfront. According to Bankrate:

“. . . you might qualify for a first-time homebuyer loan or assistance. First-time buyer loans typically have more flexible requirements, such as a lower down payment and credit score. Many help buyers with closing costs and the down payment through grants and low-interest loans.”

To find out more, talk to your state’s housing authority or check out websites like Down Payment Resource.

Expand Your Options by Looking at Condos and Townhomes

Right now, there aren’t enough homes for sale for everyone who wants to buy one. That’s pushing home prices up and making affordability tight for buyers. One way to deal with that issue and find a home right now is to consider condos and townhomes. Realtor.com explains:

“For many newbies, it might just be a matter of making a shift toward something they can better afford—like a condo or townhome. These lower-cost homes have historically been a stepping stone for buyers looking for a less expensive alternative to a single-family home.”

One reason why they may be more affordable is because they’re often smaller. But they still give you the chance to get your foot in the door and achieve your goal of owning a home and building equity. And that equity can help fuel your move into a larger home later on if you decide you need something bigger in the future. Hannah Jones, Senior Economic Analyst at Realtor.com, says:

“Condos can help prospective homebuyers who perhaps have a smaller budget, but who are really determined to get a foothold in the market and start to accumulate some equity. It can be a really great entry point.”

Consider Pooling Your Resources To Buy a Multi-Generational Home

Another way to break into the market is by purchasing a home with friends or loved ones. That way you can split the cost of things like the mortgage and bills, to make it easier to afford a home. According to Money.com:

“Buying a home with another person has some obvious advantages in the mortgage department. With two incomes in the mix, buyers can likely qualify for a larger mortgage — a big help in today’s high-cost market.”

Bottom Line

By exploring first-time homebuyer assistance, condos, townhomes, and multi-generational living, it can be easier to find and buy your first home. When you’re ready, let’s connect.

Chances are at some point in your life you’ve heard the phrase, home is where the heart is. There’s a reason that’s said so often. Becoming a homeowner is emotional.

So, if you’re trying to decide if you want to keep on renting or if you’re ready to buy a home this year, here’s why it’s so easy to fall in love with homeownership.

Customizing to Your Heart’s Desire

Your house should be a space that’s uniquely you. And, if you’re a renter, that can be hard to achieve. When you rent, the paint colors are usually the standard shade of white, you don’t have much control over the upgrades, and you’ve got to be careful how many holes you put in the walls. But when you’re a homeowner, you have a lot more freedom. As the National Association of Realtors (NAR) says:

“The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.”

Whether you want to paint the walls a cheery bright color or go for a dark moody tone, you can match your interior to your vibe. Imagine how it would feel to come home at the end of the day and walk into a space that feels like you.

Greater Stability for the Ones You Love Most

One of the hardest things about renting is the uncertainty of what happens at the end of your lease. Does your payment go up so much that you have to move? What if your landlord decides to sell the property? It’s like you’re always waiting for the other shoe to drop. Jeff Ostrowski, a business journalist covering real estate and the economy, explains how homeownership can give you more peace of mind in a Money Geek article:

“Homeownership means you are the boss and have the biggest say in your lifestyle and family decisions. Suppose your kids are in public school and you don’t want to risk having them change schools because your landlord doesn’t renew your lease. Owning a home would remove much of the risk of having to move.”

A Feeling of Belonging

You may also find you feel much more at home in the community once you own a house. That’s because, when you buy a home, you’re staking a claim and saying, I’m a part of this community. You’ll have neighbors, block parties, and more. And that’ll give you the feeling of being a part of something bigger. As the International Housing Association explains:

“. . . homeowning households are more socially involved in community affairs than their renting counterparts. This is due to both the fact that homeowners expect to remain in the community for a longer period of time and that homeowners have an ownership stake in the neighborhood.”

The Emotional High of Achieving Your Dream

Becoming a homeowner is a journey – and it may have been a long road to get to the point where you’re ready to take the plunge. If you’re seriously considering leaving behind your rental and making this commitment, you should know the emotions that come with this owning a home are powerful. You’ll be able to walk up to your front door every day and have that sense of accomplishment welcome you home.

Bottom Line

A home is a place that reflects who you are, a safe space for the ones you love the most, and a reflection of all you’ve accomplished. Let’s connect if you’re ready to break up with your rental and buy a home.

CONNECT

AREAS SERVED

SOLANO | NAPA |SONOMA

SACRAMENTO | LAKE | MARIN COUNTIES

Made with ❤️ © 2023 NAVI